In a nutshell

German e-commerce is not booming – but it is clearly back on a growth path. In 2025, online sales grew by 3.9% to €92.3 billion, slightly above the previous year’s 3.8% growth. The market is becoming broader and more stable: all categories grew, FMCG accelerated strongly, marketplaces remained dominant, and Amazon gained share again. At the same time, Temu, Shein, TikTok Shop, Amazon Haul, AI and second-hand commerce show how quickly the competitive logic of German online retail is changing.

⏱ Time to Read: appr. 8 min

German e-commerce is back on the (cautious) growth track

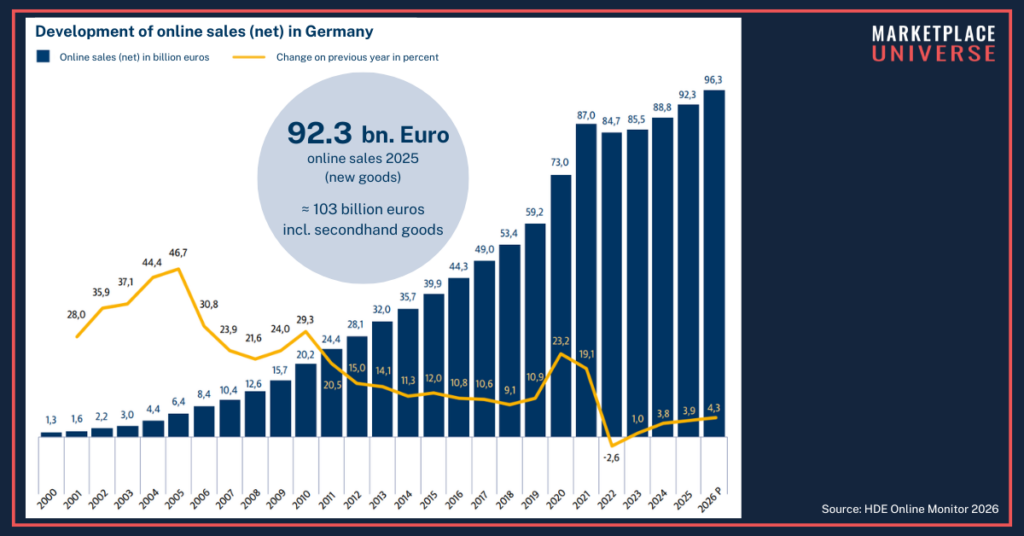

After the difficult post-pandemic years, German e-commerce has found its rhythm again. According to the new HDE Online Monitor 2026, online retail sales in Germany grew by 3.9% in 2025, reaching €92.3 billion net. That follows growth of 3.8% in 2024 and marks a further step away from the correction phase of 2022 and 2023.

For 2026, the HDE expects the market to grow by another 4.3%, reaching €96.3 billion. That is not a return to pandemic-style acceleration. But it is a steady recovery – and probably the healthier kind. Since 2020, German online sales have increased by €19.3 billion.

The more interesting question is where this growth comes from. Last year, the headline was simple: marketplaces drove the entire growth. This year, the story is more nuanced. Marketplaces are still ahead, but the gap to other online formats has narrowed.

All categories are growing again

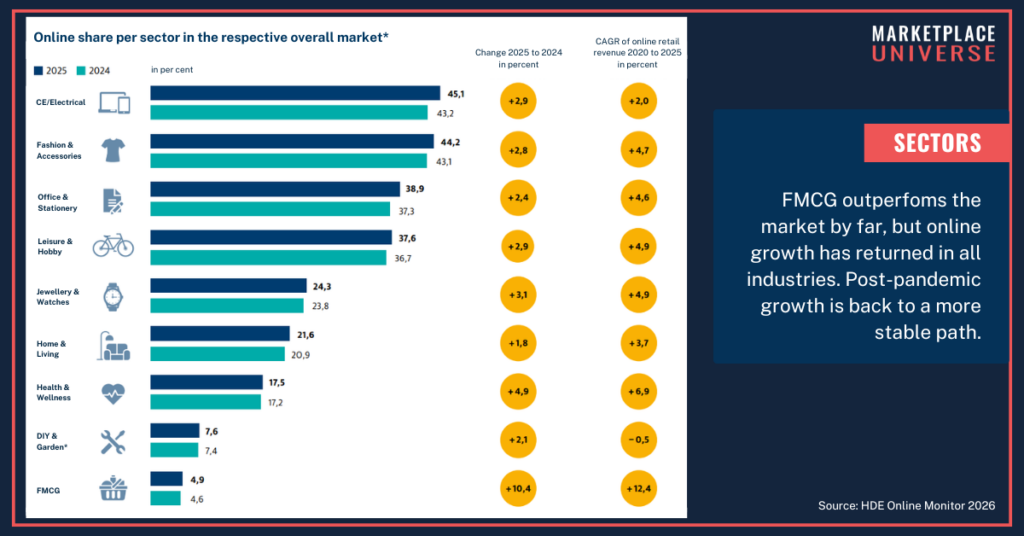

For the second year in a row, all major online retail categories recorded growth. The striking part: growth rates have moved closer together. The weak patches of previous years, especially in categories like fashion, seem to be largely over.

The clear exception is FMCG. Online sales of fast-moving consumer goods grew by 10.4% in 2025 – more than 2.5 times the market average. In 2024, FMCG was already the fastest-growing category with 7.3%. This year, the category pulled even further ahead.

Other categories grew at a much more moderate pace: Health & Wellness by 4.9%, Jewelry & Watches by 3.1%, Consumer Electronics and Leisure & Hobby by 2.9% each, Fashion & Accessories by 2.8%, Office Supplies by 2.4%, DIY & Garden by 2.1%, and Home & Living by 1.8%.

Fashion and Electronics remain Germany’s two largest online categories. Fashion & Accessories reached €21.2 billion, accounting for 22.9% of total online sales. Consumer Electronics followed with €19.7 billion, or 21.3% of the market. Together, the two categories still make up 44.2% of German online retail – but their combined share is slowly declining. In 2024, it stood at 44.7%.

FMCG is the category to watch. Its share of total online sales rose from 13.7% to 14.5%, reaching €13.4 billion. The online penetration is still low, but the direction is clear: groceries, drugstore products and everyday consumer goods are becoming a much more important part of German e-commerce.

Marketplaces still lead – but they no longer own the whole growth story

In 2024, the message was brutal for many retailers: all online growth came from marketplaces, while other online channels declined. In 2025, the picture looks less one-sided.

Sales via marketplaces and platforms grew by 5.4%. That is still above the total online market growth of 3.9%. But other formats also grew: providers with online DNA by 3.9%, stationary retailers by 4.0%, and manufacturers by 3.8%.

So yes, marketplaces remain the strongest growth format. But the simplistic “marketplaces win, everyone else loses” narrative no longer works. Own shops, retailer shops and manufacturer-led models are not dead. They just need a much clearer role: brand experience, customer relationship, loyalty, better margins, exclusive assortments – something beyond simply listing products online.

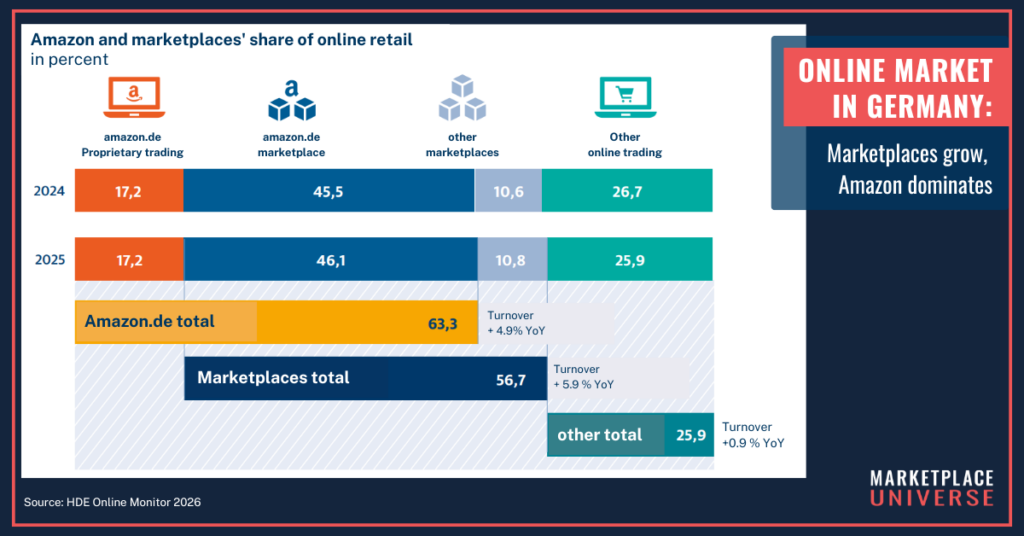

Germany remains an Amazon market.

According to the HDE Online Monitor 2026, Amazon.de accounted for 63.3% of German online sales in 2025, up from 62.7% in 2024. Amazon’s own retail business remained stable at 17.2%, while the Amazon marketplace grew from 45.5% to 46.1%.

That may sound like a small increase. It is not. When a player already controls more than 60% of the market, even half a percentage point matters.

Other marketplaces also gained slightly. The combined share of marketplaces outside Amazon – including eBay, Zalando/About You, Otto, TikTok Shop and specialist platforms such as ManoMano, Moebel.de or Chrono24- rose from 10.6% to 10.8%. Overall, marketplaces accounted for 56.7% of German online sales in 2025.

The uncomfortable truth remains: Germany is not a highly fragmented marketplace market. It is an Amazon-dominated market with a relevant, but much smaller, platform landscape around it.

Temu and Shein are big – but not as big as you think

Temu and Shein are now structurally relevant in Germany. The HDE estimates their combined German sales at around €4.7 billion in 2025, up from roughly €3.0 billion in 2024. That equals about 5% of total German online retail.

That is impressive. But it is not market takeover.

The two platforms are large enough to put pressure on pricing, assortment expectations and customer acquisition. But they are still far from Amazon’s scale. The industry sometimes talks about Temu and Shein as if they had already rewritten the entire German market. The numbers are more sober: they are a serious force, not the whole market.

Their user base is growing, though. The HDE estimates that 16.0 million people in Germany bought from Temu and/or Shein in 2025, up from 14.4 million in 2024. Average order value rose sharply from €24.95 to €34.15, while order frequency increased slightly to 8.51 orders per year.

The reputation problem remains. Many non-buyers still associate Temu with poor product quality. But among actual buyers, the picture is more positive. That is the real risk for established players: Temu does not need to convince everyone. It only needs a large enough group to keep buying frequently.

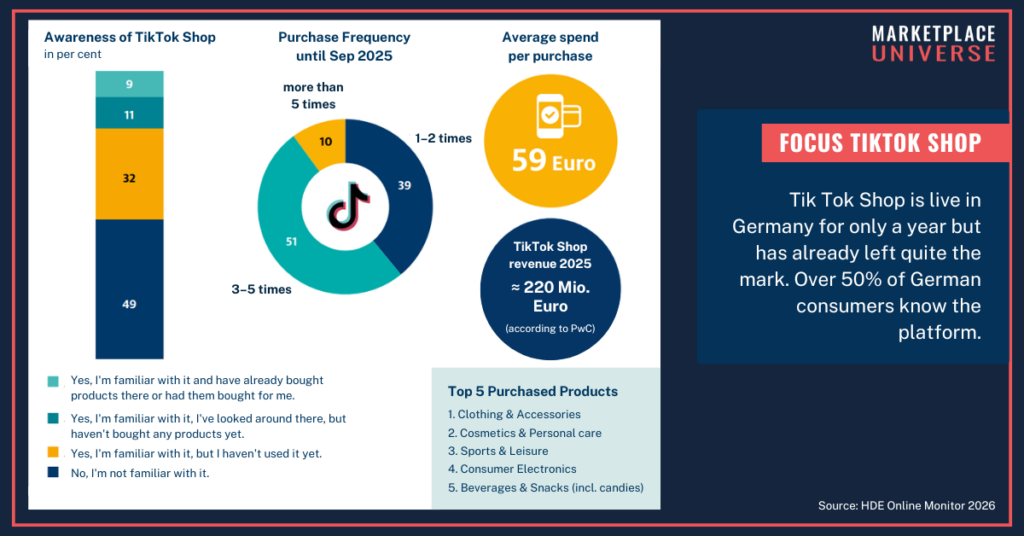

TikTok Shop starts small – but not quietly

TikTok Shop is still tiny compared with Amazon, Zalando or even Temu and Shein. But the early numbers are worth watching.

Half a year after launch, 52% of German internet users already knew TikTok Shop, and 9% had already bought there. The top categories were Clothing & Accessories, Cosmetics & Care, Sports & Leisure, Consumer Electronics, and Drinks & Snacks. Average spending per purchase was €59, and PwC data cited by the HDE estimates TikTok Shop’s German 2025 sales at around €220 million.

That does not make TikTok Shop a must-have channel for every brand yet. But ignoring it would be lazy. Especially in categories where impulse, creators, entertainment and low-friction buying meet, TikTok Shop is becoming part of the platform conversation faster than many expected.

Amazon Haul brings the low-price fight into Amazon’s own ecosystem

The low-price battle is no longer just happening on Temu, Shein or AliExpress. Amazon is moving too.

Amazon Haul launched in Germany in June 2025. Four months later, it already had 47% awareness, 13% of respondents had purchased via the concept, and 59% of buyers ordered at least once a month.

This matters because Amazon Haul brings ultra-low-price mechanics into the most powerful commerce ecosystem in Germany. For brands and sellers, that means the pressure from low-price models is no longer somewhere else. It is moving closer to the mainstream.

Cross-border shopping keeps rising

German consumers are also becoming more comfortable buying from abroad. The share of online shoppers who say they consciously order from foreign providers increased from 24% to 26%. China remains by far the most important source country: 49% of those who bought abroad ordered from China.

This is one of the reasons why national market logic is becoming weaker. German brands and retailers are not only competing with German retailers anymore. They are competing with global supply chains, platform-funded reach, aggressive pricing and increasingly frictionless cross-border delivery.

Social media and AI are moving into the shopping journey

The customer journey is becoming less predictable. Social media is not just a place for inspiration anymore. It triggers purchases. On average, 13% of German internet users have bought a product after seeing it in a person’s social media post. Among 30- to 39-year-olds, the share reaches 23%.

AI is moving even faster into product research. 35% of consumers already use AI chatbots when researching products, mainly to compare product features, quality and prices.

For brands, this is more than a marketing side note. Product data, reviews, trust signals, price logic and content quality are becoming machine-readable sales assets. If shoppers start asking AI tools what to buy, where to buy it and which shop to trust, visibility will no longer depend only on Amazon search, Google rankings or marketplace filters.

Second-hand is now a €10.5 billion online market

Second-hand is still excluded from the HDE’s main online sales figure because the report focuses on new goods. But as a market, it has become too large to treat as a niche.

Online second-hand sales reached €10.5 billion in 2025, up 5.3% from the previous year. Since 2019, the market has grown from €5.7 billion, with a CAGR of 10.6%.

The strongest segments are Books, Fashion & Accessories and Consumer Electronics. What started as a sustainability story is increasingly also a price story. Consumers buy second-hand not only because it feels responsible, but because it helps reduce spending. That makes the market relevant far beyond vintage fashion or refurbished electronics.

Conclusion: Germany’s online market is stable – but the rules are shifting

The German online market is growing again. Not spectacularly, but steadily. That alone is good news.

But the real story is not the growth rate. It is the changing structure underneath.

Marketplaces remain the backbone of German e-commerce, and Amazon has strengthened its already dominant position. But the market is no longer as one-sided as last year’s figures suggested. Other formats are growing again, FMCG is becoming a stronger online category, second-hand is reaching serious scale, and low-price platforms are forcing everyone to rethink price perception and customer expectations.

At the same time, TikTok Shop, social commerce and AI-driven product research are changing how products are discovered and evaluated. The next phase of German e-commerce will not be won only through more listings, more ad spend or more marketplace presence. It will be won through better execution: sharper channel roles, cleaner data, stronger pricing discipline, operational excellence and a realistic understanding of where customers actually make decisions.

Germany is not in an e-commerce boom. But it is entering a more complex, more platform-driven and more competitive phase of online retail.

Key Learnings

- German e-commerce is growing steadily again: Online sales increased by 3.9% to €92.3 billion in 2025, with 4.3% growth forecast for 2026.

- FMCG is the strongest growth category: With 10.4% growth, FMCG is pulling far ahead of the market average, even though online penetration remains low.

- Marketplaces remain dominant, but the gap is narrowing: Marketplace sales grew by 5.4%, still above market average, but other online formats are growing again too.

- Amazon is still the central force in Germany: Amazon.de increased its share to 63.3% of German online sales, driven mainly by its marketplace business.

- Temu and Shein are serious, not all-powerful: Their estimated combined market share reached around 5%, making them releva- but not dominant.

- TikTok Shop and Amazon Haul show where the pressure is moving: Social commerce and ultra-low-price mechanics are entering the mainstream faster than many brands expected.

- Second-hand has become a structural market: At €10.5 billion, online second-hand is no longer a side topic.

- AI will reshape product discovery: If consumers use AI tools for product research, brands need better data, clearer trust signals and more machine-readable product content.

If you’d like to learn more about TikTok Shop, check out our in-depth guide How to Succeed on TikTok Shop or our podcast Just Being on TikTok Shop Is Not Enough: Philips’ 2-Year Playbook for Europe #LTM153

Enjoyed this article? The Marketplace Universe Weekly is our free newsletter – every Monday, the latest marketplace news, platform updates, our newest posts, and the insights that matter, delivered straight to your inbox. So you never miss a thing. 👉 Subscribe here: https://marketplace-universe.com/newsletter/