In a nutshell

Wish once defined the first wave of China-to-consumer marketplaces in Western markets, reaching more than 100 million monthly users and shipping products to over 100 countries, as disclosed in ContextLogic’s IPO filings. Temu later entered the market with a strikingly similar formula of ultra-low prices, direct manufacturer access and aggressive marketing — yet scaled far beyond its predecessor. Why was one successful where the other one failed? A tale of two Chinese marketplaces.

⏱ Time to Read: appr. 6 min

When Wish became a global meme

For a few years, Wish defined how Western consumers experienced Chinese e-commerce. The platform became a meme, a shopping app and a global marketplace at the same time — reaching more than 100 million monthly users and shipping products to over 100 countries.

Then, almost as quickly as it had risen, it disappeared. And as Wish was fading from the spotlight, a new platform emerged that looked strikingly familiar: Temu.

- Same pricing logic.

- Same supply chains.

- Same aggressive marketing.

But while Wish collapsed, Temu scaled. Somewhere along the way, their trajectories diverged. But where?

The rise — and quiet disappearance — of Wish

Wish was founded in 2010 by Piotr Szulczewski and Danny Zhang and operated by the San-Francisco-based company ContextLogic, the technology company behind the marketplace.

Szulczewski, a former Google engineer, designed Wish not as a traditional online shop, but as a mobile discovery platform. Instead of searching for products, users scrolled through an endless feed of algorithmically recommended items — an experience closer to social media than to classic e-commerce.

Behind this interface sat a large cross-border marketplace connecting Western consumers directly with merchants, most of whom were based in China. This structure enabled extremely low prices and rapid assortment expansion.

For a time, the model scaled: According to ContextLogic’s SEC filings around the company’s 2020 IPO, Wish reached more than 100 million monthly active users globally and operated in over 100 countries.

But the decline came quickly. User numbers dropped from over 100 million to roughly 74 million within a short period after the IPO, according to subsequent ContextLogic filings. As marketing spend was reduced, traffic followed. What initially looked like massive scale proved to be fragile.

In 2024, ContextLogic exited the business entirely, selling the Wish marketplace to Singapore-based e-commerce group Qoo10 for approximately $173 million, as reported in the company’s 2024 annual disclosures.

Today, Wish still exists under Qoo10 ownership — but at a dramatically smaller scale. According to ECDB projections, the platform’s GMV may reach around €43 million by 2026, a fraction of what its early trajectory once suggested.

The question is why such a large platform lost relevance so quickly.

The cracks in the model

Several structural weaknesses of the Wish model became visible over time.

Dependence on paid growth

Wish invested heavily in digital advertising to drive app installs and traffic. When marketing spend declined, user numbers dropped almost immediately. The platform struggled to convert initial attention into sustained engagement.

Erosion of trust

The meme culture surrounding Wish reflected a deeper issue: inconsistent product quality, misleading listings and long delivery times. The humor generated visibility — but also defined the brand.

A fragile logistics model

Wish relied heavily on direct cross-border shipping from Chinese merchants to Western consumers. This resulted in long delivery times and complex returns. While the company attempted to improve logistics, the model remained fundamentally cross-border.

More importantly, this approach would have struggled under today’s conditions. Rising tariffs, stricter customs enforcement and geopolitical tensions have made ultra-cheap cross-border shipping significantly more complex — putting pressure on exactly the structure Wish depended on.

Limited marketplace evolution

Wish never developed into a broader marketplace ecosystem. Initiatives such as Wish Local were discontinued, and the platform struggled to attract a meaningful base of international sellers. The merchant structure remained largely China-centric, limiting its ability to evolve into a more resilient global marketplace.

By the time the company attempted to address these issues, momentum was already lost.

Temu — another marketplace as “bought on Wish”?

When Temu entered Western markets, the similarities were hard to ignore. The platform combined three core elements that had already defined Wish:

- extremely aggressive marketing

- ultra-low prices

- direct manufacturer access.

Both platforms connected Western consumers directly with Chinese supply chains. Both scaled through visibility. And both positioned themselves around price. Yet Temu did not simply repeat the model — it extended it. The platform has already reached more than 75 million monthly users in the EU, qualifying as a Very Large Online Platform under the Digital Services Act, according to the European Commission.

Where Temu corrected Wish’s weaknesses

Temu entered the market with a model that looked similar to Wish — but addressed the same structural challenges more systematically.

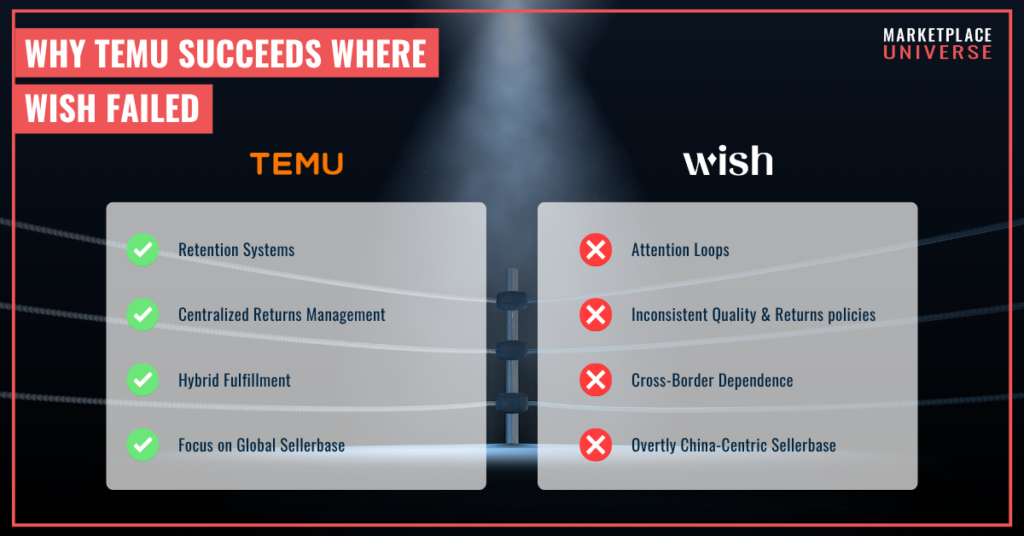

From attention loops to retention systems

Wish relied on behavioral triggers such as endless scrolling and flash deals to drive impulse purchases. These mechanisms optimized for attention. Temu builds on this logic with more explicit gamification systems — including rewards, incentives and repeat-visit triggers — designed to increase retention and frequency.

From unmanaged inconsistency to controlled risk

Both platforms struggle with trust. But while Wish let merchants handle customer complaints with widely different outcomes, Temu manages them more systematically through centralized policies, refund mechanisms and tighter platform control. The problems remain — but are less visible to the customer.

From cross-border dependence to hybrid fulfillment

Wish remained fundamentally dependent on direct China-to-consumer shipping. Temu, by contrast, is actively transitioning toward hybrid fulfillment models that combine cross-border supply with regional warehousing and local inventory.

This shift is partly strategic and partly reactive. Rising tariffs and stricter trade controls have made pure cross-border models harder to sustain. Temu has responded by building infrastructure that Wish never developed.

From a China-centric seller base to a gradually global marketplace

While both platforms started with a heavy focus on China-based merchants, Temu managed to evolve from that and is actively expanding its seller base to include European and American merchants. This transition is still ongoing — but marks a clear strategic shift.

The difference in scale reflects this evolution. ECDB data highlights the scale of this divergence: Temu could reach around €110.6 billion in GMV by 2026, while Wish is expected to remain at roughly €43 million.

A divergence that reshaped the China marketplace narrative

After all, Wish and Temu did not quite represent the same marketplace model. Wish built a viral discovery app that connected Western consumers with Chinese merchants — but failed to build the infrastructure required for long-term growth.

Temu started from a similar foundation, but evolved into a much more complex global platform. The difference lies less in pricing than in execution and evolution. While Wish mostly stayed true to its nature, Temu simply managed to adapt.

But it is also important to consider the historical context when comparing the two. Because Temu is not just executing better — it is also operating under conditions that force a more mature version of the same model. Conditions that Wish did not experience during their prime.

The result remains: in global marketplaces, scale alone is not enough. Infrastructure decides who survives.

Key Learnings

1. Viral growth does not guarantee platform stability

2. Logistics is becoming a structural advantage

3. Marketplace success depends on seller diversity

4. Trust is not solved — it is managed

5. Execution matters more than the model

25.03.2026 – Written by Ricarda Eichler, Journalist and Author for OHN