In a nutshell

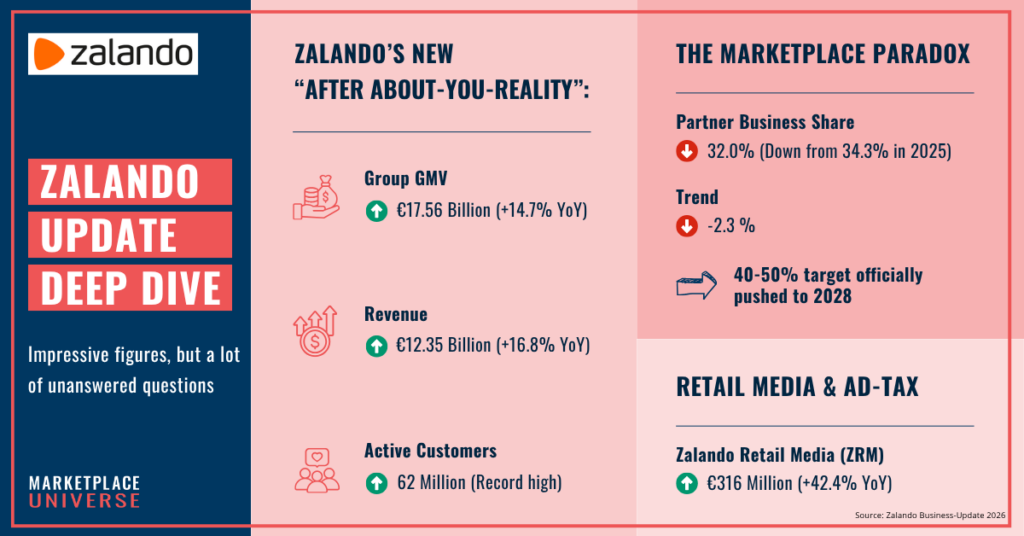

Zalando’s 2025 results (reported in March 2026) look strong at first glance: €17.56 billion GMV, double-digit growth, and a scaled “Fashion Duo” with ABOUT YOU. But beneath the surface, the structure of that growth is shifting. The declining Partner Program share, accelerating Retail Media revenues, and deeper integration of logistics and software point toward a more tightly orchestrated ecosystem. At the same time, many of the most critical questions for brands — around partner dynamics, commercial terms, and future dependencies — remain unanswered in the current reporting.

⏱ Estimated reading time: 6 minutes

Zalando Deep Dive 2026: How Zalando is Reshaping its Platform Model

For years, Zalando was often described as a company transitioning from a traditional retailer to a platform. However, the 2025 results show that Zalando has long outgrown this simple binary. It is no longer a question of “retailer or marketplace”—it is about building an interconnected commerce infrastructure.

Through the merger with ABOUT YOU, a “Fashion Duo” has emerged that offers brands enormous reach while at the same time increasing their exposure to a more tightly integrated ecosystem.

1. The Growth Equation: Organic vs. Integration

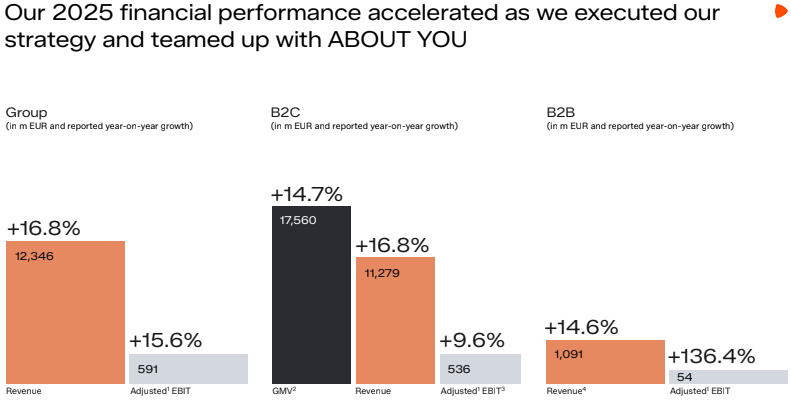

Zalando reports strong figures: €17.56 billion GMV (+14.7%) and €12.35 billion revenue (+16.8%). With 62 million active customers, the group reaches a significant share of fashion consumers in Europe.

Marketplace Universe Insight

These figures need to be read in the context of the ABOUT YOU integration. Since ABOUT YOU contributed approximately 5.5 months, organic GMV growth sits at roughly 9%. This remains a strong result in a challenging market environment, but it also suggests that growth is increasingly driven by consolidation and market depth rather than purely organic expansion.

2. The Partner Program Paradox: Dilution or Strategic Shift?

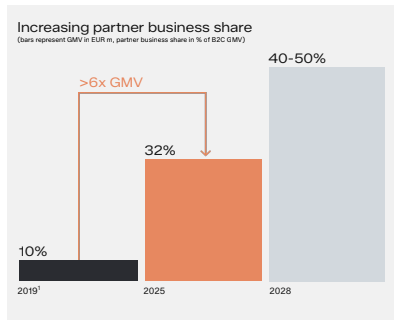

One of the most relevant metrics is the Partner Program share (32%) of B2C GMV. Compared to 34.3% in 2024, this appears to be a decline. However, the integration of ABOUT YOU plays an important role, as the group average is mechanically diluted.

Marketplace Universe Insight

Zalando highlights a comparison to 2019 (6x increase) instead of focusing on the year-over-year change. At the same time, the 40–50% target has been pushed to 2028, which raises a broader question: is Zalando currently rebalancing toward wholesale — or preparing to expand the Partner Program again under a different structure?

For brands, the key question is not only how the Partner Program evolves, but how it will be positioned within a broader Zalando + ABOUT YOU ecosystem.

3. Power Concentration: What do the €40m Synergies actually mean?

A central element is the €40 million annual cost synergies (2026). From an investor perspective, this signals efficiency. From a market structure perspective, it may point toward increasing consolidation.

If Zalando and ABOUT YOU move closer together in terms of systems, processes, and potentially commercial logic, this could lead to a shift in negotiating power over time. With Zalando and ABOUT YOU representing two of the most important fashion platforms in Europe, brands are increasingly operating within a shared ecosystem.

4. The Levi’s Watershed: The Trojan Horse named SCAYLE

The deal with Levi’s is the strategic highlight of the report. Levi’s is utilizing SCAYLE (Zalando’s B2B shop software) to handle its entire global Direct-to-Consumer (DTC) business across the U.S., Canada, and Europe.

Marketplace Universe Insight

Zalando is positioning itself at the infrastructure layer of e-commerce. For brands, this expands Zalando’s role from a sales channel to a technology provider. SCAYLE implies a level of technological integration beyond a marketplace listing and may also signal a broader B2B expansion into the US market, even if the report does not yet provide full clarity on how these capabilities will evolve.

5. ZEOS: From a Service Offering to a Strategic Lever

ZEOS enables around €11 billion GMV for 1,200+ partners, underlining its growing role within Zalando’s ecosystem. With increasing scale, logistics integration is becoming more central.

At the same time, ZEOS can also serve additional marketplaces, positioning it as part of a broader infrastructure layer rather than just a Zalando-specific service. This expands its strategic relevance for brands operating across multiple channels.

However, this also introduces a different type of dependency. Brands that rely heavily on ZEOS are increasingly exposed to logistics cost structures, where changes in pricing or service conditions can directly impact margins, particularly once processes are deeply embedded.

6. Retail Media: The Rising “Visibility Layer”

Retail Media has grown by +42.4% to €316 million, indicating that paid visibility is becoming more important within the platform.

For brands, this does not necessarily replace organic performance, but maintaining and scaling visibility may increasingly require advertising investment. At the same time, the combination of Retail Media, ZEOS, and other platform requirements may put pressure on margins, even without direct changes to commission rates.

What the Annual Report DOES NOT tell us

Despite the depth of the data, several of the most important questions for brands remain unanswered. The report provides scale and direction — but offers only limited visibility into how the system will evolve in practice.

1. True Partner Program Dynamics

How has the Partner Program actually developed post-integration? The report aggregates Zalando and ABOUT YOU in a way that limits comparability. This makes it difficult to assess whether the underlying marketplace model is strengthening, stagnating, or structurally changing.

2. Harmonization of Terms

Will commercial conditions, fees, and access rules converge between Zalando and ABOUT YOU over time? As both platforms grow closer operationally, brands are increasingly exposed to the possibility of aligned terms — but the report provides no indication of how this might evolve.

3. System Dependencies

How deeply will services like SCAYLE and ZEOS become embedded in brand operations? The Levi’s example highlights the potential, but it remains unclear how tightly these components will be connected — and what that means for flexibility and independence.

4. The Role of Logistics in Platform Performance

Could logistics integration (e.g. via ZEOS) become a stronger factor in visibility, performance, or program access? The report highlights operational improvements, but does not clarify whether logistics will evolve into a more structural requirement.

5. AI and Brand Identity

Zalando reports that a large share of onsite content is supported or generated by AI tools. While this increases efficiency, it raises questions about how platform-generated content and individual brand identity will be balanced over time.

6. Assortment and Stock Allocation Power

As Zalando and ABOUT YOU increase their combined importance for many brands, a more structural question emerges: who will shape assortment decisions in the future?

If brands rely on both platforms across wholesale and partner models, platform demand and buying decisions could begin to influence not only distribution, but also production planning. This would mark a shift from platforms as sales channels toward platforms as indirect drivers of assortment strategy.

Conclusion

Zalando is expanding across multiple layers of commerce — from consumer demand to logistics and software infrastructure. At the same time, key questions around terms, control, and dependencies remain unresolved.

For brands, success is no longer just about assortment, pricing, or execution. It increasingly depends on navigating a broader ecosystem with evolving rules.

What is already clear, however, is that the strategic importance of Zalando + ABOUT YOU is increasing — while visibility into how this system will evolve remains limited.